Whether or not to use UTII is a personal matter for each taxpayer. If a positive decision has been made, then it is mandatory registration with the tax service. Accordingly, in the event of a transition from UTII to another taxation regime, the entrepreneur must notify the tax authority about this officially.

Voluntary refusal of UTII is possible in following cases:

- The activity on the “imputation” has ceased, for example, the taxpayer has ceased to provide services, or his activity has been excluded from the list of services suitable for this regime by a decision of the territorial authority.

- A different taxation system has been chosen.

What is this document and why is it needed?

The taxpayer’s advantage is that when calculating and paying tax imputed income is used, the amount of actual profit received is not taken into account.

If a decision is made to switch to another taxation system, the entrepreneur is required to prepare an application. Form UTII-3 is suitable for an organization, form UTII-4 is suitable for an individual entrepreneur.

Applications for termination of activities in accordance with the imputed tax system must be submitted to the tax office in accordance with the place of registration.

Application and withdrawal deadline

It is possible to remove an organization or individual entrepreneur only if there is an appropriate basis.

Such a basis may be the termination of the imputed activity. To do this, you need to submit an application to the tax office. The period of official notification to the control body is limited 5 working days. The deregistration date is the date specified in the application.

After the response from the Federal Tax Service, the enterprise does not have the right to use this system to calculate payments to the budget.

The procedure for filling out UTII-3 and UTII-4 forms

The UTII-3 application includes certain fields that must be filled out, unless otherwise stated in the rules.

Every number indicated in a separate cell. The exception is the date, which is filled in 3 fields separated by a dot.

Both manual and computer filling are allowed.

When filling out a declaration on a paper form The following conditions must be met:

- Blue or black pen for entering all necessary information.

- Text, numeric and code values are filled in from left to right, starting from the very first cell.

- All text must be written in capitals. printed letters.

- Each empty field must be filled with a dash.

If the company has chosen cocomputer filling method, for printing you should set the Courier New font, height 16-18.

A few general rules for filling out applications:

- It is prohibited to use proofreaders or other similar means to correct errors.

- The form can only be printed on one side of the sheet.

- If the application consists of several sheets, they are not allowed to be stapled.

Fields TIN and KPP are required when filling out application No. UTII-3.

There may be several checkpoint codes in accordance with the number of territories used to conduct “imputed” activities.

If we are talking about a Russian enterprise, then in lines 5-6 you should indicate the number 35, and if about foreign ones - 77.

Field "Tax authority code" necessary to indicate the code of the tax office that accepts applications.

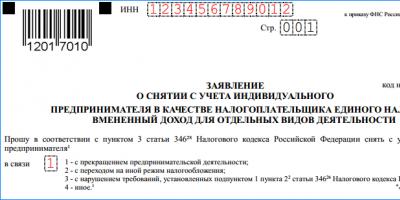

Next you need indicate the reason for deregistration(Clause 3 of Article 346.28 of the Tax Code of the Russian Federation) in a single cell:

- “1” – termination of activity;

- “2” - transition to another taxation system;

- “3” - violation of the requirements for the use of UTII established in paragraphs. 1 and paragraphs. 2 clause 2.2. Art. 346.26 Tax Code of the Russian Federation;

- “4” is a different reason.

In the next cell you need to put numbers:

- “1” - if we are talking about a Russian company;

- “2” - if about a foreign enterprise.

In the four lines below, You must write the full name of the institution. In this case, one should rely on the constituent documents.

After this, the OGRN is indicated.

Specially designated fields DD.MM.YYYY must be used for indicating the date of termination of activity, but only if the basis for deregistration is the number 1, 2 or 4.

If the company committed violations of Art. 346.26 of the Tax Code of the Russian Federation (clauses 1 and 2 of clause 2.2), then you just need dashes in these cells.

In addition, you must indicate:

- number of application pages;

- information about the representative submitting the application and a copy of the document confirming his authority;

- Contact details;

- date and signature.

The sequence of filling out attachments to the UTII-3 form depends on what kind of papers they are. Their list determines the types of activities that the organization has practiced and plans to discontinue.

The TIN and KPP fields are identical to those located on page 1. Entrepreneurial activities are further specified.

This is followed by information about the addresses of activities that were subject to UTII, and everything ends with the manager’s phrase confirming the accuracy and completeness of the information provided.

Filling out an application on the UTII-4 form cannot be called complex, but it still has some features. The document includes 2 sections: a title page and several appendices.

The first (title) part includes:

- Personal data of an individual entrepreneur (full name, INN, OGRNIP).

- Reason for withdrawal.

- The date of termination of work in accordance with the “imputed” tax.

- Number of attached papers.

- Representative contact details.

- Date and signature.

In applications, the number of which directly depends on the number of types of business being closed, you must indicate:

- entrepreneurial activity (code);

- the exact address;

- IP signature.

On one sheet of the application it is permissible to indicate no more than three types of activities, generating income.

What happens if you fail to submit your application on time?

Since 2013, in accordance with the new norm, a UTII payer who has violated the deadline for filing an application aimed at terminating (suspension) of activities must indicate the last day of the month in which the application was submitted. The payer will need to pay for the full month, not for the actual time of activity.

The single tax on imputed income does not provide for filing a “zero declaration”, since the base profitability is taken as the object of taxation. The tax amount for the quarter is calculated from the date of registration or until the date of deregistration.

You can find out how to close the UTII tax in the video below.

Legislation for entrepreneurs provides for several types of preferential tax regimes, which include UTII. All of them are used voluntarily. Therefore, individual entrepreneurs can periodically change taxation systems in order to reduce the tax burden. In addition, in connection with the future abolition of UTII (2018), many entrepreneurs are gradually leaving it.

IP may stop using imputation for the following reasons:

- The type of activity located on UTII is no longer carried out.

- Closes the business.

- The criteria for applying this regime have been violated.

- The tax regime is being changed.

The Tax Code of the Russian Federation establishes that an entrepreneur must, within five days, send to the Federal Tax Service an application for withdrawal if he stops using this regime. For this document, a special UTII form 4 was established by order of the Federal Tax Service. To fill it out, you can use Internet services and programs for filling out reports. An individual entrepreneur can also purchase a UTII-4 form at a printing house or print it from a computer and fill it out by hand.

An individual entrepreneur sends an application for deregistration of UTII to the tax office at the place where the activity is carried out, in person, through an authorized representative. It is possible to send the UTII-4 form via mail or electronic communication channels.

Termination of the use of imputation begins from the date specified in the document, from the last day of the month in which there was a violation of the requirements for the use of UTII, the moment of transition to the new regime.

An individual entrepreneur must remember that in some cases, changing UTII to another preferential regime (for example,) can be done at the end of the year. If this is carried out during it, then most likely the entrepreneur will be forced to apply the general taxation system. Therefore, it would be more appropriate to postpone the decision on the transition until the end of the year.

After receiving the application in the UTII-4 form, the Federal Tax Service must, within five days, remove the individual entrepreneur as a taxpayer by imputation and send him a written notification about this.

If an entrepreneur worked in this mode in several municipalities, then applications must be submitted to each Federal Tax Service Inspectorate at the place of business. Also, if an individual entrepreneur completely decided not to use UTII, but he used it for two or more types of activities, all of them must be indicated in the application.

Sample of filling out UTII-4

At the top of the document, the entrepreneur’s TIN of 12 characters is indicated. A little lower, on the right side of the sheet under the form number, enter the 4-digit code of the tax service to which the application is sent.

Then you need to indicate the reason why the entrepreneur is deregistered under UTII:

Then you need to indicate the reason why the entrepreneur is deregistered under UTII:

- Code “1” is set if he completely ceases any business activity.

- Code “2” - if he is going to switch to using another tax system.

- Code “3” is used if, during the implementation of the activity, the conditions for the use of the imputed system were violated - the number of hired workers exceeded 100 people.

- Code “4” - in other cases, for example, if the entrepreneur continues to work, but closes the type of activity for which UTII was applied.

After this, you must indicate your full name without abbreviations. All empty cells in this field are crossed out.

After this, you must indicate your full name without abbreviations. All empty cells in this field are crossed out.

On the next line enter the OGRNIP code. After it is entered the date from which the entrepreneur wants to deregister.

Under it you need to indicate the number of sheets of applications, with a breakdown of the types of activities. In addition, if an application to the tax office is submitted by an authorized representative, then it is necessary to indicate on how many sheets of documents confirming his rights are attached.

In the next block, which is divided into two parts, the entrepreneur enters data only on the left. It indicates who submits the completed form - the entrepreneur himself (code “1”) or his representative (code “2”). In the second case, you need to enter his full name. and TIN. Then the contact phone number is written down, a signature is placed and the date of completion. If the document is submitted by a representative, then it is necessary to indicate the name of the document confirming his rights. All empty cells must be marked with a “-”.

On the application sheet, you can enter three activity codes by which deregistration occurs. If there are more such types, then you can use additional pages.

On the application sheet, you can enter three activity codes by which deregistration occurs. If there are more such types, then you can use additional pages.

In each one, you must also enter the full address at which it was sent. All empty cells in all blocks are crossed out. At the end of the page you need to put a signature that confirms that the data in the document is correct.

In each one, you must also enter the full address at which it was sent. All empty cells in all blocks are crossed out. At the end of the page you need to put a signature that confirms that the data in the document is correct.

This form of taxation, as we already noted in the article, is in second place in popularity among individual entrepreneurs after the simplified tax system. Having chosen the taxation system “single tax on imputed income”, register as a UTII taxpayer and submit an application for registration as an individual entrepreneur no later than five days from the start of work.

Carefully read the instructions for filling out and the sample, then download the current form and fill in the required data. If you have any questions, feel free to write them in the comments, we will answer them promptly. This is what it looks like completed UTII form-2…

Form and sample application for UTII application

Sample of filling out UTII-2 for individual entrepreneurs in 2016

Remember, that:

- Registration of an individual entrepreneur as a taxpayer of imputed tax takes 5 days.

- After this time, the INFS receives a notification about the application of the selected system. It is unlawful to demand documents other than the application.

- The start date for calculating the imputed tax will be the date specified in the application.

- Payments can be calculated using.

How to fill out UTII-2 correctly

The document consists of two sheets: Title and Appendix.

The taxpayer's title page contains the Taxpayer Identification Number, Unified State Register of Individual Entrepreneurs (USRNIP) number, full name, and start date of activity. The Federal Tax Service code is indicated in abbreviation - the first four digits. The individual entrepreneur signs the application personally and puts 1 or 2 if the paper is handed in by a representative. In the latter case, additionally indicate the full name, telephone number, and powers of the authorized representative.

Application, in addition to the TIN and page numbering, we fill in the type of business to be opened: code, address. One sheet contains three types of activities (retail outlets with different addresses). If more codes and addresses are declared, then additional sheets of the Appendix are filled out.

Preparation of an application for the use of UTII with a form dated 2016 updated: November 30, 2018 by: Everything for individual entrepreneurs

An application in form No. UTII-3 is sent to the tax service in order to notify it of the temporary suspension of the organization’s activities. These applications can only be submitted by legal entities. For individual entrepreneurs, there is another form under the number UTII-4.

The application for deregistration of an organization from the UTII register is very simple and understandable, consisting of only one form and an appendix to it. The application reflects information about the type of activity of the organization in relation to which the payment of temporary tax is completed.

Dear readers! The article talks about typical ways to resolve legal issues, but each case is individual. If you want to know how solve exactly your problem- contact a consultant:

APPLICATIONS AND CALLS ARE ACCEPTED 24/7 and 7 days a week.

It's fast and FOR FREE!

The UTII-3 application must be submitted no later than 5 working days after the cessation of any activity, as well as when replacing the temporary regime of activity with any other general or simplified form.

In case of untimely submission of this application to the tax service, the obligation to pay tax will remain in any case, even if the organization’s operation ceases, since imputed income is subject to taxation in all cases, since it does not depend on the real income of the organization and its actual activities.

Basic Rules

The form consists of one title page. and the company's checkpoint should be written at the top of the form. Next, you need to reflect the code of the tax department to which the application is sent. Then the next line indicates the full name of the organization, which corresponds to.

At the top of the form there is a field in which you must enter the reason for completing the work. From the proposed options, select the appropriate one and enter the number of the correct answer.

The reasons may be the following:

- the organization ends its business activities;

- the organization switches to another taxation regime;

- the organization violated the requirements that must be met when working in an imputed mode.

The company can be Russian or... You must select the correct designation and enter it in the form with a number. Russian companies should also indicate their OGRN.

The most important thing is to enter the date from which the organization should be exempt from paying taxes on imputed income. In addition, if the applicant is represented by an authorized representative, then the number of documents indicating this must be indicated on the title page.

In the power of attorney information section, fill in all the information about the authorized person and TIN, if known. Below you should write the contact number of the founder of the organization, by which, if necessary, you can contact him.

The second sheet of the document is called the appendix. It indicates the type and type of activity of the organization. Only three types of work can be claimed as tax exempt in the application. If you need more, you should fill out additional applications. The business activity code and the legal address of the organization are also placed there.

All application forms for deregistration of an organization from UTII must be signed and sent to the tax service where the company was registered. You can submit documents in person, by coming to the tax office, or by sending an email and using.

Definition and applications

UTII is a tax regime that will be in effect until 2019. The essence of this regime is that the calculation and payment of tax bills occurs in accordance with the income imputed to it, which is established in an article of the Tax Code.

It is worth considering that the actual income received by the organization does not play any role. The peculiarity of the single tax is that the taxpayer independently makes decisions related to issues of its application.

Since last year, the cadastral value of real estate has been subject to taxation, but there is still no property without a cadastral value. Individual entrepreneurs must understand that according to UTII, only the property that is necessary for carrying out business activities is subject to taxation.

The object of taxation is usually called income that is the result of the declared type of activity. It is calculated taking into account all the necessary conditions that can affect the methods and methods of its production.

UTII can be applied in addition to other already existing taxation systems. For example, together with general or simplified modes.

Paying a single tax on imputed income makes an entrepreneur free from paying many other taxes, which include, for example, value added tax, that is, VAT. Management in such organizations is carried out in the most usual way, as in other companies with other tax regimes.

The cadastral value of real estate is the main indicator when calculating property taxes, but it is important to take into account the tax rate, which is established by local governments in regulations.

Application form for deregistration of an organization from UTII registration:

Reasons and standard terms

When a person conducts business activities, he may encounter a situation where it will be more profitable for him to remove his company from the UTII register than to continue paying taxes under this regime.

The reasons for this can be very different:

| An organization ceases to conduct activities that are subject to certain taxes on imputed income. | In this case, you must be extremely careful, because if the organization is not registered under the simplified taxation system at the time of sending the application to remove the company from UTII, then the organization will automatically be subject to general taxation, which will have a negative and very difficult impact on small businesses. But the transition to another tax system is only possible no earlier than next year. |

| During the development of business, a situation arose that did not allow the application of uniform taxation on imputed income in accordance with the law | For example, the entrepreneur’s retail space expanded by more than one hundred and fifty square meters or twenty new work cars were purchased. According to the legislation of the Russian Federation, it has become possible to switch to a simplified taxation system, without having to wait for the next calendar year. |

| An entrepreneur, analyzing the expenses made and the income generated, sees that the use of UTII is ineffective for his business activity | However, in this case, the founder faces one problem. If this decision was made, for example, in May, then the entrepreneur can de-register UTII and switch to another taxation system only with the onset of the new year, namely from the first year. Until this moment, he will have to pay taxes according to the UTII system, regardless of whether it is unprofitable or not. |

When an entrepreneur decides to remove a company from UTII for reasons that do not imply that this statement will come into force only at the beginning of the new year, then from the moment of termination of his activities he is given five working days to notify the tax service about this.

Document forms

The transition to taxation of imputed income since 2013 has been carried out voluntarily. All organizations and individual entrepreneurs are required to contact the tax authorities at the place where their activities are carried out, that is, where the company’s legal address is registered.

The Federal Tax Service has developed forms for registration or deregistration for both various organizations and individual entrepreneurs. In addition, she also established procedures for filling out these forms.

There are four forms of documents for UTII:

| Form No. UTII-1 | This is an application for registration of an organization as a single tax payer on imputed income for certain types of activities. |

| Form No. UTII-2 | This is an application for registration of an individual entrepreneur as a single tax payer on imputed income for certain types of business activities. |

| Form No. UTII-3 | This is an application to deregister an organization as a single tax payer on imputed income for certain types of activities. |

| Form No. UTII-4 | This is an application for deregistration of an individual entrepreneur as a single tax payer on imputed income for certain types of business activities. |

Procedure algorithm

The deregistration procedure involves an application procedure. This means that the taxpayer himself is obliged to contact the tax service with the appropriate application within the specified time. The date of termination of payment of this tax in this case is the date of termination of activity in this area.

However, what should be understood by termination of activity:

- The founder ceases to work with a single tax on imputed income. Consequently, the taxpayer must contact the relevant authority within five days after completing business activities. From that moment on, he officially ceases to use UTII.

- Local authorities have excluded any type of business activity from the taxation system, which falls under UTII. In this case, the five-day period is counted from the date of official entry into force of the relevant normative act, that is, from the first day of the first month of the quarter in which the document and resolution were published.

To deregister, organizations must use the application form UTII-3, and individual entrepreneurs - UTII-4. After the founder submits the application, the tax service must consider it within five working days and within the same period notify the taxpayer of his deregistration from the UTII register. These notifications are also sent using certain forms.

If the five-day deadline for filing an application has been violated, the tax service will remove it from the register and send a notification only on the last day of the month.

After this, the organization or individual entrepreneur stops paying UTII, but there is another obligation behind them. They must file a tax return and pay all tax bills. Therefore, in order to reduce payments, you should contact the tax service as early as possible.

Order and sample

The reason code for registration for payment of a single tax on imputed income and the individual taxpayer number are indicated at the top of the form. Then below is the code assigned to the tax service and consisting of four characters. Next, the number indicates the reason for deregistration: 1 - at your own request, 2 - due to a transition to another taxation system, 3 - as a result of violation of UTII requirements, 4 - for other reasons.

Then you need to set the end date of the activity, and also indicate how many sheets the application contains. If the application is filled out not by the founder personally, but by his authorized representative, then his rights must be documented and indicated on the form.

In the application you also need to indicate the TIN and KPP of the organization and select three types of occupations; if there is a specific need, you can use additional application forms. All sheets must be signed, last name, initials and their decoding. Unfilled blocks should be crossed out.

Sample of filling out an application for deregistration of an organization from UTII registration:

Receiving paper

As mentioned above, it is necessary to notify the tax service within five days from the date of termination of activities subject to taxation under the UTII system.

In 2019, the obligation of taxpayers to report to the tax service, where the organization was registered for a single imputed tax, about changes in the type and place of activity was not established.

Taxes and calculation procedure

UTII can be reduced if the founder has made all mandatory contributions, that is, pension and social security for persons who are temporarily unable to work (the birth of a woman’s child, injuries). Another method is used only when employees have sick leave.

However, it is necessary to take into account a number of rules:

- The tax amount cannot be reduced by more than fifty percent. So, when the amount of payments exceeds UTII, the maximum tax reduction can be done only by half.

- When reducing due to sick leave, you must keep in mind that only those paid for by the employer are considered. Additional payments for sick leave in the amount of the average daily salary are also not grounds for a tax reduction.

- UTII is reduced only for contributions made in the current quarter.

The single tax on imputed income is calculated using the following simple formula:

Tax base = basic profitability of the organization * the value of the actual indicator for three months * coefficient - deflator * adjustment coefficient.

The resulting tax base value should be multiplied by fifteen percent.

How to correctly fill out an application for deregistration of an organization from UTII registration

The application form in a single copy must be filled out exclusively with a ballpoint pen, blue or black ink and only in block letters. You must be very careful and especially pay attention to the writing style, because if some letters look like capital letters, the application may not be accepted and you will have to fill out the form again.

Of course, the most convenient way to do this is on a computer, having first downloaded the required Excel form. You need to install the Courier New 16, 18 point font on your computer or laptop, then fill out all the fields and print. It’s easier to correct this way and they won’t find fault with the writing, especially since the use of proofreaders is strictly prohibited.

In addition, the letter can be sent electronically, which is now quite common. If necessary and if any questions arise, the tax service will contact the entrepreneur.

Possible fines

If the taxpayer has not applied for deregistration of the single tax on imputed income within five working days, then he is obliged to pay this type of tax until the end of the year, regardless of the date of termination of any activity. In addition, the taxpayer may be subject to a fine of 200 rubles for late submission of documents.

If such a situation occurs, the entrepreneur should not send zero reporting to the tax service, since it may be regarded as an attempt by the taxpayer to evade paying taxes. And this, in turn, is subject to more serious punishment. That is why it is so important to contact the tax organization in a timely manner.

In conclusion, it is worth noting all the pros and cons of this taxation system. When an organization does not receive income recorded every month, it is in a disadvantageous financial position, and paying UTII aggravates the situation.

Despite this, if the organization expands and begins to receive more income, it is not subject to additional taxation, and the company clearly benefits from this. However, it is worth noting that in any case, the most beneficial for entrepreneurs is a simplified taxation system.

Attention!

- Due to frequent changes in legislation, information sometimes becomes outdated faster than we can update it on the website.

- All cases are very individual and depend on many factors. Basic information does not guarantee a solution to your specific problems.

The preferential tax regimes, according to existing legislation, include a system in which a business entity pays. For a variety of reasons, persons registered as individual entrepreneurs may decide to stop using this regime. To do this, you need to submit an application to the Federal Tax Service to deregister the individual entrepreneur’s UTII.

The current rules of law determine that an entrepreneur must be deregistered as a UTII payer within five days from the date of termination of activity or transition to another taxation system.

To do this, the individual entrepreneur must send a tax application, for which the UTII-4 form is provided. LLC uses for these purposes.

An entrepreneur may stop using imputation for the following reasons:

- Termination of the area of activity in which the UTII system was installed.

- Closing the individual's individual entrepreneurial activity as a whole.

- Violation of the criteria for using the UTII system.

- Changing the tax system used to another.

Attention! If an entrepreneur decides to change the applicable regime, he must take into account that the use of the new taxation system in some cases is possible only from the beginning of the year.

Therefore, a situation may arise that the individual entrepreneur left the imputation, but, for example, could not switch to it. In this case, it will automatically have .

Having received this application, the tax office must consider it within five days, and at the end of this period, issue a notice to the entrepreneur about the closure of the UTII.

Where to apply

An application for withdrawal from UTII must be submitted to the Federal Tax Service where the individual entrepreneur was previously registered as a UTII payer, that is, at the place of previously carried out activities.

In this case, the UTII-4 form must be filled out at each tax office if activities carried out in several municipalities have been discontinued.

When an entrepreneur closes several types of activities, but within the boundaries of one city, locality, etc., he can combine withdrawals for each of them in one application.